There comes a time in the business founder’s life to consider selling some equity in the company, if not to dispose it all. Reasons for the sale are always situational. The sale could arise from the need to expand capacity of the business, sustain or dispose of it entirely to realise a return on investment. Disposal could also be owing to the need to meet other pressing financial obligations.

Many factors influence company equity valuations. Thus in selling equity, how best can owners avoid suffering from seller’s remorse just as buyers do after their priced purchases? By Nimroth Gwetsa, 30 April 2016.

Founders are sometimes reluctant to sell equity in their company. Perhaps they perceive the sale as “losing” control of their company. The thought of having to defer leadership decisions and responsibilities to others is perhaps the reason for their reluctance. In this era of staff empowerment, diversification and talent management, it is normal for different incentive schemes to be devised for such employees. Incentives for high contributing executives and talented staff might include giving away company equity.

The reluctance of small-business owners in selling equity might deny their companies opportunities to grow to larger higher revenue yielding companies. When owners decide to sell, the sale is often done under duress and when the company is about to foreclose. Selling when the company has had prolonged period of poor financial performance may result in the owner not controlling the sale and company equity valuation.

Selling equity to realise business growth can best be achieved when the sale is not forced, but the owner has planned for it beforehand and has had enough time evaluating potential equity partners.

With more preparation and knowledge of company valuations, owners may limit after sale regrets.

Learn about Importance of Being Knowledgeable, Prepared and Principled

“My people are destroyed for lack of knowledge” – Hosea 4:6 ESV. Lacking knowledge in company and product valuations would automatically increase the owner’s vulnerability, placing them at the mercy of buyers who would be eager to determine the selling price for them.

“The simple believes everything, but the prudent gives thought to his steps” – Proverbs 14:15 ESV. Having knowledge shouldn’t be about collecting facts, but having a thorough understanding of the company’s situation, facts about equity sale and valuations. This includes understanding implications of selling company equity. The analysis should then inform the sale decision.

“Desire without knowledge is not good, and whoever makes haste with his feet misses his way” – Proverbs 19:2 ESV. Once information has been analysed and the sale decision made, owners should not rush to conclude the deal until they have allowed that decision to sink in before being carried out. I’m not advocating that decisions be over analysed. Owners should allow their decisions to fester in the mind for a little while. This allows issues that might have been overlooked to arise.

“The prudent sees danger and hides himself, but the simple go on and suffer for it” – Proverbs 22:3 ESV. Once the decision has festered for a short while, owners should spend time identifying and analysing issues that might be unfavourable if the final sale decision was to be executed. Given the gravity of the decision, there should be no contesting or contradictory or outstanding thoughts and issues suppressed and left unresolved. Owners need to ensure that they have correctly and adequately answered all unresolved concerns and issues. Answers to those unresolved issues would help owners overcome any feelings of regret afterwards. Since regret and remorse are feelings, they are resolved by decisions made on the soundness and principles of answers to issues causing the rise of those feelings.

“O simple ones, learn prudence; O fools, learn sense” – Proverbs 8:5 ESV. Buyer’s remorse is often caused by feeling short-changed. No one, even a fool, wants to look and be left feeling foolish. To be content with the price given, owners should surround themselves with trustworthy experts in valuations. But they should do their homework and own calculations so they could have sound basis for their expectations.

“The simple inherit folly, but the prudent are crowned with knowledge” – Proverbs 14:18 ESV. Ultimately, there is no one size fits all determination of the price. As in all other buyer and seller interactions, the sale depends on desperation of the parties involved. Desperation determines the ultimate price of the sale.

These proverbs show the importance of knowledge. After sale regrets can be minimised with more knowledge and enables the seller to secure a better price for equity sold.

Understand Factors Affecting Company Valuations

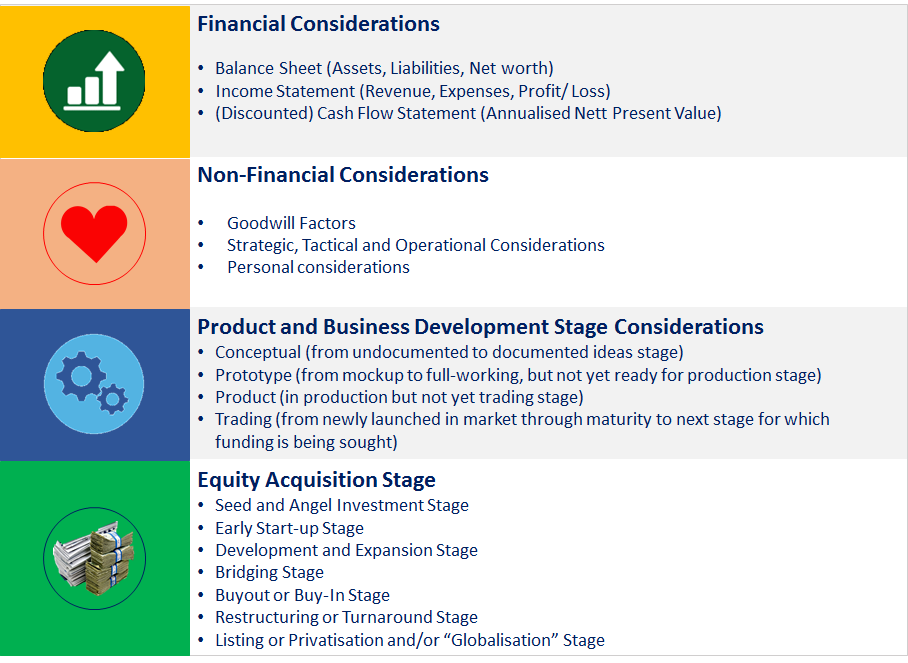

In non-forced or desperate sales, financial and nonfinancial considerations play a major part in finalising the valuation of company equity as show diagrammatically below.

Some factors affecting equity valuation

More specifically, other factors influencing equity valuations include geographic location of the company or market, market and industry type, funding and funding source types, competitors and nature of competition, risk and return trade-off over investment period, capital structure and quantum, investment attractiveness, leadership, management and workforce capacity, ownership and tangibility of intellectual property, technology, customers and reputation of the company.

Know How To Calculate Non-Forced Equity Sale Percentage Ownership for Given Investment Capital

Successful deals are those promoting mutual benefits. Good sellers would thus be concerned about the value the buyer would derive from the sale and not only about what they, as sellers, would earn. Failure to consider value for the other side could result in acrimonious sale, including seller’s remorse afterwards. Buyers have many choices to invest their capital. Equity sold by owners competes with other market offerings. Investors would buy seller’s company equity on the belief that investing in those companies would give them better returns than market offerings for similar levels of risk.

To this end, owners as sellers should strive to understand value of returns buyers can expect to receive over the investment period or at exit from investing in their company.

Seen from a seller’s perspective, future value of returns (FV) against expected relative internal rate of return (IRR) and period of investment (P) are some factors they would consider in laying out their investment capital, present value (PV), to buy company equity.

But from old management school studies, we know that:

- FV =Present Value (PV) x (1+ Target IRR)P.

Future Value needs to be achievable yet sufficiently enticing for investors to buy company equity against all other available competing market offerings.

Companies in trading and having well-maintained financial records stand a better chance of receiving investment capital. Investors would be able to use this information to work out the Price Earnings Ratio (PER) for their potential investment. As investors expect the value of their company equity to increase, they may want to know what its future value would be in case they want to exit from their investment. This value is known as terminal value (TV).

To that end, we also know from old management school studies that:

- TV = PV (estimated PER).

Armed with knowledge of calculations 1 and 2 above from the buyer’s perspective, sellers need to estimate percentage equity buyers can expect to get in the company in exchange of the investment capital injected. I should warn again that those considering selling their company equity must consult their financial advisors for more professional advice on company equity valuations.

Nevertheless, to that end and from the buyer’s perspective, Percentage Equity Ownership can be determined, at least, in one of the following two ways:

- Method 1: %Equity Ownership = Required FV at exit ÷ Projected TV of company or equity at exit.

- Method 2: %Equity Ownership = PV of investment ÷ present value of TV of the company or equity at exit, where present value of TV (TVpres) of the company or equity at exit is calculated as follows: TVpres = Projected TV at exit of company or equity ÷ FV, with value of FV as calculated in 1

The formulas for the above methods indicate how equity ownership percentage a buyer can expect to get. But these do not indicate the number of shares that sellers could give buyers for equity sold. Neither do these formulas indicate the value of future dilution due to issuing that equity or of staggering injection of investment capital or of due diligence sensitivities. I’ll stop right here to allow sellers to work out the rest. The aim was to provide an indication of what buyers might expect to enable sellers to manage expectations accordingly.

Having seen from the buyer’s perspective, the buyer should then set and manage own expectations accordingly.

Buyer’s and seller’s remorse can be avoided if parties are more knowledgeable and prepared about company equity valuations, and have reconciled in their minds the sale decision.

Without knowledge and preparation, feeling of remorse would emerge when one party starts doubting the value of the transaction they have agreed to. At worst, feelings of regret emerge when parties become aware, after the effect, of new information that would have been useful had it being known before conclusion of the sale transaction.

Realise the Benefits of Proactive Selling of Company Equity

Sellers may not always control the sale of their company equity. Circumstance, known or unforeseen, could force the sale of company equity.

Owners should avoid stubbornness and failure to realise bleak prospects of the company honouring its liabilities before being forced to sell or their company is repossessed to recoup payments for outstanding debts. When it becomes clear that the company would be in distress and there are dim prospects for recovery, it would be better to proactively start the sale of company equity than losing everything due to a forced sale.

I urge owners to arm themselves with knowledge and understanding of value from the buyer’s perspective to limit losses from forced sale. They would have no excuse, but regrets if they choose to ignore proper preparation and arming themselves with good knowledge of company equity valuations.

Sometimes proactive selling should be considered when the company cannot counter aggressive advances from competitors or their superior products eroding the company’s market share. This type of equity sale is the defensive one and can ensure the survival of the company. Nevertheless, owners should never rest on their laurels, even if their companies are dominant market players. They should innovate, embrace change, listen to their customers and staff and stay relevant. They should maintain open perspectives to be persuaded even by competition in their advances for a slice of their company’s equity. The owner’s survival and realisation of their investment returns could depend on it.

Seller’s remorse is avoidable pain. Let yours, as a seller, be a happy ending.